5 financial-related dynamics we’re grateful for

- 11.17.23

- Markets & Investing

- Commentary

Review the latest Weekly Headings by CIO Larry Adam.

Key Takeaways

- U.S. economic growth continues to outpace other G7 nations

- Strong labor market should cushion next downturn

- Disinflationary trends remain intact

On behalf of the Investment Strategy team, we extend our sincerest wishes for a Happy Thanksgiving wherever your holiday travels may take you. And this Thanksgiving is expected to be another bustling travel time, with AAA projecting over 55 million people traveling – an increase of 2.3% over the previous year. It’s easy to see why Thanksgiving is one of the most cherished American holidays – it is a time to gather with family and friends, share a hearty meal with all your favorite trimmings (I’m partial to corn-bread stuffing and green bean casserole!), and express gratitude for all the good things that happened over the last year. As we get into the spirit of Thanksgiving and reflect upon the past year, we list below five financial-related dynamics we are most grateful for:

- Resilient U.S. economy | Following the surge in inflation, the most aggressive Fed tightening cycle since the 1980s and multi-decade lows in business and consumer confidence, calls for a U.S. recession have been prevalent all year. However, a resilient consumer and strong labor market have helped the U.S. economy sidestep a recession thus far. In fact, the US economy grew at its fastest pace since 4Q21, rising 4.9% in the 3Q23. In addition, since COVID-19, the U.S. economy has been a standout relative to its Developed Market counterparts. Specifically, since the end of 2019, U.S. GDP growth has cumulatively increased 7.4%, far outpacing the next strongest G7 country (Canada: +3.5%). While we expect the U.S. economy to enter a recession in the first half of next year, solid consumer (record net worth, low debt serving costs as a % of disposable income) and corporate fundamentals should ensure that it is one of the shortest and mildest recessions going back to 1945.

- Strong labor market | The U.S. labor market continues to defy gravity and is another reason why the economy has avoided a recession up until this point. With the U.S. economy adding 8.4 million jobs over the last 24 months, more people working has helped propel consumer spending. In fact, a record 161 million Americans are now employed, above the pre-COVID-19 high of 158.5 million. Wage growth has also been healthy, with average hourly earnings increasing 4.4% over the last year – outpacing the rate of inflation (~3.2%). And with the number of job openings (9.6 million) still outpacing the total number of unemployed workers for each of the last 29 months, we expect more muted job losses relative to history during the next recession as businesses will be reticent to layoff employees given the struggle to find qualified workers in the post-pandemic period.

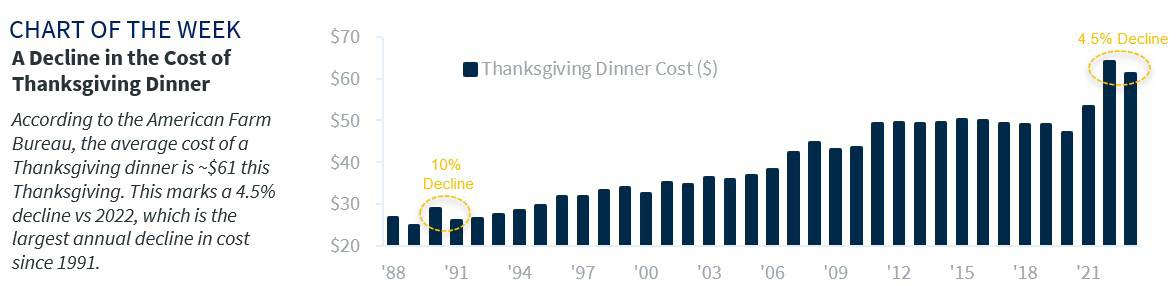

- Disinflationary trend remains intact | Inflation has cooled considerably over the last year, falling from a peak of 9.1% in June 2022 to just 3.2% currently! Easing price pressures reflect falling energy prices (-4.5% YoY), lower goods prices and more subdued transportation costs – thanks to declining used car prices (-7.1% YoY) and airfares (-13.2% YoY). It also reflects a modest easing in shelter costs, which we suspect will be major driver of further disinflationary forces as we progress into 2024. In addition, the American Farm Bureau Federation has reported that the average cost for a Thanksgiving feast for ten people will drop to $61.17 per person this year, a 4.5% decline compared to 2022. We are grateful for these disinflationary trends as it has fueled optimism (and we agree) that the Federal Reserve’s tightening cycle has likely come to an end.

- Robust equity market gains | Following the worst annual performance since 2008 (S&P 500: -18% in 2022), 2023 was the first year in two decades that strategists, in aggregate, forecasted a negative year for the S&P 500. However, we are thankful that has not occurred as the S&P 500 is on pace to rise ~20% on a total return basis (almost double the annual historical average)! Returns have been driven by P/E expansion, a result of better-than-expected growth, decelerating inflation and an incrementally less aggressive Fed. Importantly, we are most thankful for MAGMAN – the six mega-cap Tech-related names (MSFT, APPL, GOOGL, META, AMZN, NVDA). These stocks, in aggregate, are up 69% year-to-date, accounting for over 75% of the returns for the S&P 500. However, ex-MAGMAN, the S&P 500 would be up only 6%. With our view that the Fed starts cutting rates in mid-2024, inflation eases further, and interest rates move lower, additional equity market upside is likely over the next 12 months.

- The income is back in fixed income | The bond market has faced unprecedented losses over the last two years as the Fed rapidly raised interest rates to respond to rising inflation pressures. While the sharp increases in longer maturity bonds have been painful for investors – with the 10-year Treasury yield climbing to its highest level in sixteen years – there is a silver lining. Bonds now provide healthy income and some of the most compelling valuations relative to other asset classes in over a decade! The high starting level of yields is an attractive opportunity to lock-in elevated rates, particularly as history has shown that 10-year yields decline on average ~100 bps and bonds perform well on a total return basis in the 12-months following the Fed’s final rate hike.

All expressions of opinion reflect the judgment of the author(s) and the Investment Strategy Committee, and are subject to change. This information should not be construed as a recommendation. The foregoing content is subject to change at any time without notice. Content provided herein is for informational purposes only. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Past performance is not a guarantee of future results. Indices and peer groups are not available for direct investment. Any investor who attempts to mimic the performance of an index or peer group would incur fees and expenses that would reduce returns. No investment strategy can guarantee success. Economic and market conditions are subject to change. Investing involves risks including the possible loss of capital.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Diversification and asset allocation do not ensure a profit or protect against a loss.